RGD readers will know that I’m very skeptical of the reliability of government economic statistics, mostly because they are a constantly moving target that mutate over time. However, a closer look at everything from TOTLL to today’s GDP Advance (3.2% annual) makes it appear as if the statistical shenanigans are growing exponentially:

I’m concerned with these numbers – quite concerned in fact. The Federal Government borrowed (and presumably spent) $462 billion in excess of tax receipts over the first three months of 2010. But PCE – personal consumption expenditures – was up $83 billion and federal spending was up only 3.5 billion.

Where did the other $375 billion go?

Into a black hole of covering existing obligations, it appears, and the final private demand GDP deficit covered by this is almost exactly 10% (GDP for the quarter is ~3.650 trillion, so $375 billion is roughly 10% of that.)

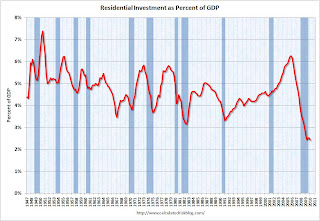

Karl Denninger isn’t the only one to notice anomalies with regards to today’s BEA release. Calculated Risk notices that Residential Investment isn’t behaving in its usual post-recessionary manner: “RI as a percent of GDP is at a new record low. And there is no reason to expect a sustained increase in RI until the excess housing inventory is absorbed. Notice that RI usually recovers very quickly coming out of a recession. This time RI is moving sideways – not a good sign for a robust recovery in 2010.”

{kind=link}