“We are seeing early evidence of that recovery: Real gross domestic product (GDP) in the United States rose an estimated 3-1/2 percent at an annual rate in the third quarter, following four consecutive quarters of decline. Most forecasters anticipate another moderate gain in the fourth quarter…. My own view is that the recent pickup reflects more than purely temporary factors and that continued growth next year is likely…. As the recovery becomes established, however, payrolls should begin to grow again, at a pace that increases over time.”

– Ben Bernanke, November 16, 2009

“Nobel Prize-winning economist Paul Krugman said he sees about a one-third chance the U.S. economy will slide into a recession during the second half of the year as fiscal and monetary stimulus fade. ‘It is not a low probability event, 30 to 40 percent chance,’ Krugman said today in an interview in Atlanta, where he was attending an economics conference. Survey of Economists Krugman’s forecast is more pessimistic than the median estimate of 58 economists surveyed by Bloomberg News in early December, which called for a 2.6 percent expansion this year following a 2.5 percent contraction in 2009.

– Paul Krugman, January 4, 2009

“I think the U.S. will avoid a double dip recession, and 2010 GDP growth will be in the 2% to 3% range.”

– Calculated Risk, January 1, 2010

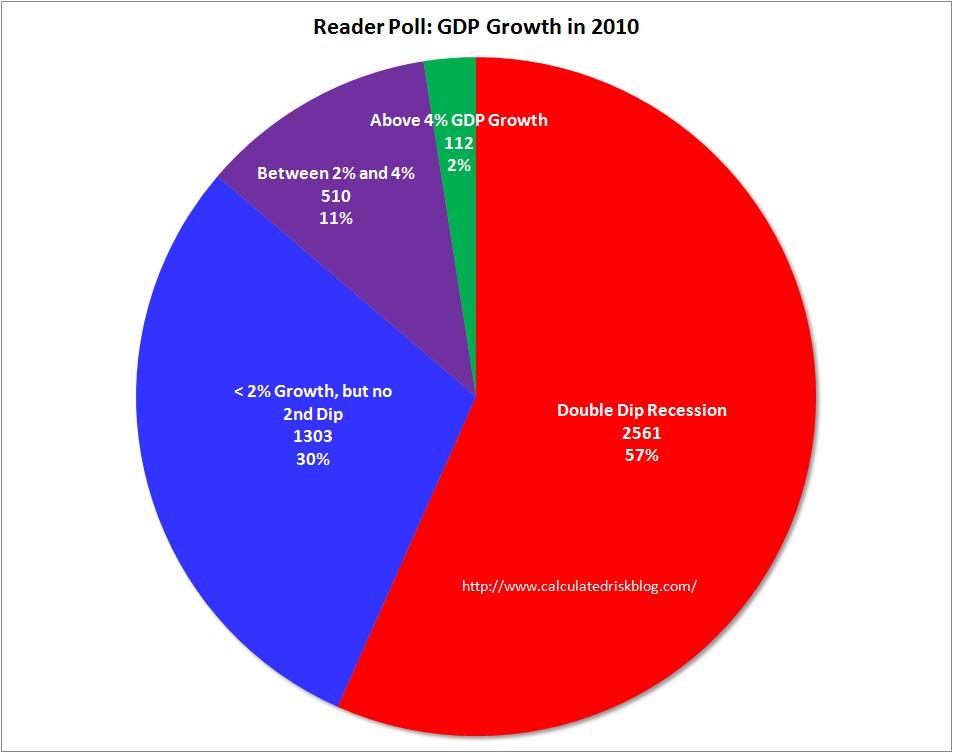

“Based on my reading, here is what I conclude the consensus views are as we head into 2010: Muted recovery, but positive growth, for sure! No risk of a ‘double dip’…. So here we are with a glorious opportunity to reintroduce Bob Farrell’s Rule 8: “When all forecasts and experts agree, something else is going to happen.”

– David Rosenberg, December 17, 2009

“Yun predicted that home prices will rise by 4 percent, while home resales, which are expected to reach 5 million this year, will surpass that level in 2010, hitting 5.7 million. Average mortgage rates will average roughly 5.7 percent, he said.”

Lawrence Yun, National Association of Realtors, November 13, 2009

“The U.S. economy next year will turn in its best performance since 2004 as spending perks up and companies increase investment and hiring, says Dean Maki, the most-accurate forecaster in a Bloomberg News survey. The world’s largest economy will expand 3.5 percent in 2010, according to Maki, the chief U.S. economist at Barclays Capital Inc. in New York.”

– Dean Maki, Barclays Capital, December 28, 2009

“Jan Hatzius, chief U.S. economist at Goldman Sachs Group Inc. in New York, who was No. 1 among forecasters of GDP during the 12 months through June 2009. Hatzius, 41, estimates the economy will expand 2.4 percent in 2010…. Hatzius and the economists at Goldman Sachs project the unemployment rate will average 10.3 percent next year, compared with a median estimate of 10 percent for 58 responses in this month’s survey.

-Jan Hatzius, Goldman Sachs, December 28, 2009

“Neal Soss, 60, chief economist at Credit Suisse in New York projects the economy will grow 3.3 percent next year.”

– Neal Soss, Credit Suisse, December 28, 2009

“John Lonski, 58, chief economist at Moody’s Capital Markets Group in New York, was No. 3. He sees a 2.7 percent expansion.”

– John Lonski, Moody’s Capital Markets Group, December 28, 2009

“Robert MacIntosh, chief economist at Boston-based Eaton Vance Management forecasting growth of 3.5 percent, and that the jobless rate will average 9.5 percent.”

– Robert Macintosh, Eaton Vance Management, December 28, 2009

“Roubini sees a greater chance of a U-shaped economic recovery in developed economies, with a 20 percent to 25 percent chance of a double-dip.”

– Nouriel Roubini, October 11, 2009

Here are seven predictions concerning economic-related events I expect to see by December 31, 2010:

1. The BLS will report U-3 unemployment to be in excess of 11 percent. The actual number of unemployed workers will be much higher.

2. The BEA will report real GDP to be less than 12,973 in billions of chained 2005 dollars. A “double-dip recession” will be the official description, but rumors of a “second great depression” will be increasingly heard as the evidence mounts that a single large scale economic event is taking place.

3. The Federal budget deficit for 2010 will exceed the projected $1.17 trillion.

4. More than 200 banks will be seized by the FDIC. Their deposits will represent more than two percent of all U.S. bank deposits. (Specific calculation: 305 banks and 5.2% of total deposits.)

5. Commercial bank loans and leases (TOTLL) will fall below $6.3 trillion.

6. All sectors credit market debt outstanding, which is published in the Fed’s quarterly Z1 Flow of Funds Accounts, will fall below $52 trillion. This will mostly be the result of continued deleveraging by the financial sector, and to a lesser extent, the housing sector, which between them will decline by more than $1 trillion.

7. The national median existing-home price will not rise 4% from $172,600 to $179,500 as predicted by NAR’s lead economist Lawrence Yun, but will fall below 165k instead. And if there is the sort of crash that is implied by the preparations for SuperTARP, existing home prices will collapse below $140k.

I also expect an increase in Sitemeter-recorded visits to the blog to increase from 1,942,640 in 2009, (161,887 per month) to 2,250,000, primarily as a result of an increased interest in economic matters. The 1.9 million visits, (3,115,071 page views), was up 19.6% from the visits 1,566,254 in 2008. I still find it astonishing that so many people continue to be interested in my various thoughts and opinions, but thank you for stopping by and please feel free to do so throughout the year.

{kind=link}