As the new year kicks off, I’ve been trying to think of a way to explain the present economic situation in a simple and graphical manner that would not only illustrate the precarious nature of the US economy, but also explain my negative perspective on its prospects as well as the positive GDP reports and expectations on the part of mainstream economists. After wasting a fair amount of time poring over the usual BEA and BLS reports, I realized that because my analyses are primarily predicated upon debt, the only thing that made sense was to go back to the Fed’s quarterly Z1 report and look more closely at the sector data. I have to confess that when the third quarter report came out a few weeks ago, I was surprised it did not show more contraction in the third quarter; total credit market debt only declined a further $113 billion from the revised Q1 2009 peak of $52.9 trillion. The net contraction to date has only been 0.53%, which seemed weirdly small when the 8.7% contraction in commercial bank loans over the same period was taken into account.

But a look at the various credit sectors usefully clarifies this apparent dichotomy. As the chart below shows, household debt reached its peak in the third quarter of 2008 and is down 1.75% since then. The financial sector began reducing its outstanding debt a quarter later than the households, but is deleveraging much faster as its debt has fallen 5.93% from the Q408 peak. Corporate debt has remained essentially flat since 2008, but the Federal government has, for the time being, been able to fill in the entire credit gap by increasing its outstanding debt by nearly one-third, 30.1%, in the four quarters since Q308! State and local government debt has also increased, but by close to an order of magnitude less at 3.25%. So, the reason we have not yet seen any significant effects of the debt-deleveraging in the household (-$242.8 billion) and financial (-$873.7 billion) sectors in the wider economy is because the Federal government has taken on an additional $1,743.4 billion of debt plus another $72.4 billion from the state and local governments to counter that contraction of credit.

So, the questions raised by this analysis are: a) can the various levels of government continue to increase their outstanding debts faster than household, corporate, and financial debts decline, b) how long can the various levels of government continue to increase their debts, c) when will household, corporate, and financial debt stop contracting? As of today, January 1st, 2010, the answers appear to be: a) No, the disparity of debt levels renders this impractical, if not impossible, especially since the early data indicates that household and financial debt is still declining. b) Probably not beyond the second quarter of 2010. State and local tax revenues fell precipitously in 2009, many state and local governments are already on the verge of bankruptcy and the White House is already talking about attempting to reduce the 2010 deficit. c) given the growing number of mortgage and credit card payments reaching 60 and 90 days late, there is no sign of this happening in 2010. In fact, much of the 2009 contraction that should have happened due to foreclosures and defaults has not yet been recorded on the books thanks to the extend-and-pretend policy presently in place.

The White House and the Federal Reserve are gambling that the contraction of household and financial sector debt will end before time runs out on their ability to increase Federal debt enough to compensate for that contraction. But despite a panoply of credit-creation programs, changes to accounting laws, and regulatory easing, they are running out of time and there are still no signs of any further appetite for debt on the part of consumers or financial institutions. The brief uptick in total bank loans from the middle of October to the middle of November has already given back its gains; TOTLL was still down 8.01% as of the most recent report on December 16th. Therefore, I conclude that the White House already knows it lost its credit gamble, which is why it is now preparing the $4 trillion SuperTARP bill known as HR 4173.

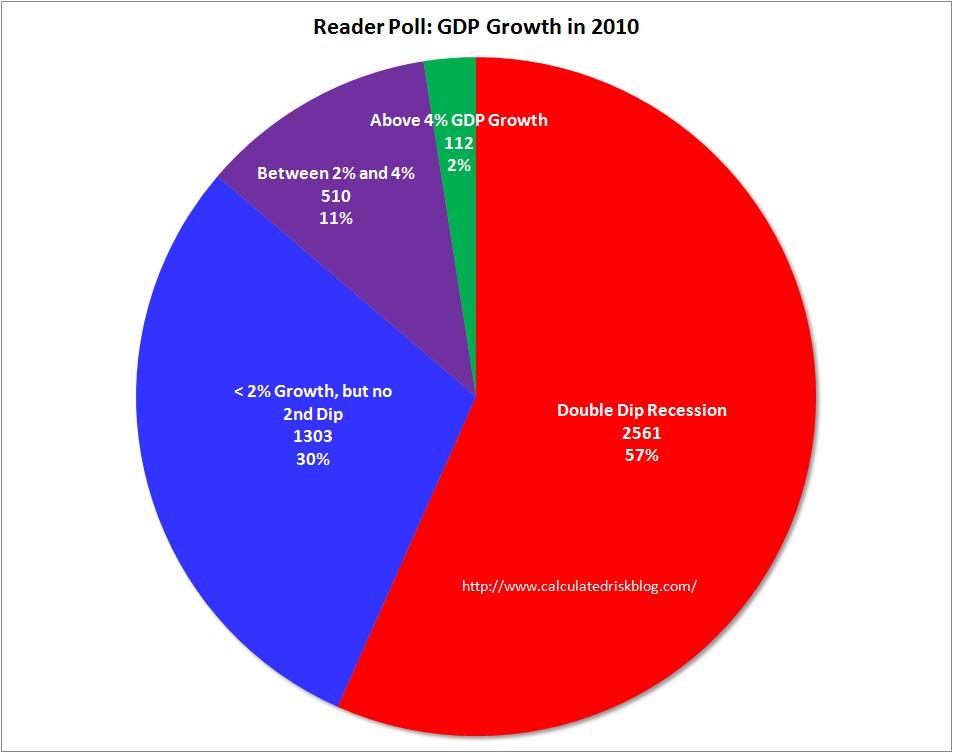

Calculated Risk’s readers would appear to share my pessimism regarding the 2010 outlook, as 57% expect the economy to fall back into contraction.