Lest you wonder why I was confident enough to take such a firm position with the title of the new book:

This OCC and OTS Mortgage Metrics Report for the second quarter of 2009 provides performance data on first lien residential mortgages serviced by national banks and federally regulated thrifts. The report covers all types of first lien mortgages serviced by most of the industry’s largest mortgage servicers, whose loans make up approximately 64 percent of all mortgages outstanding in the United States. The report covers nearly 34 million loans totaling almost $6 trillion in principal balances and provides information on their performance through the end of the second quarter of 2009 (June 30, 2009)….

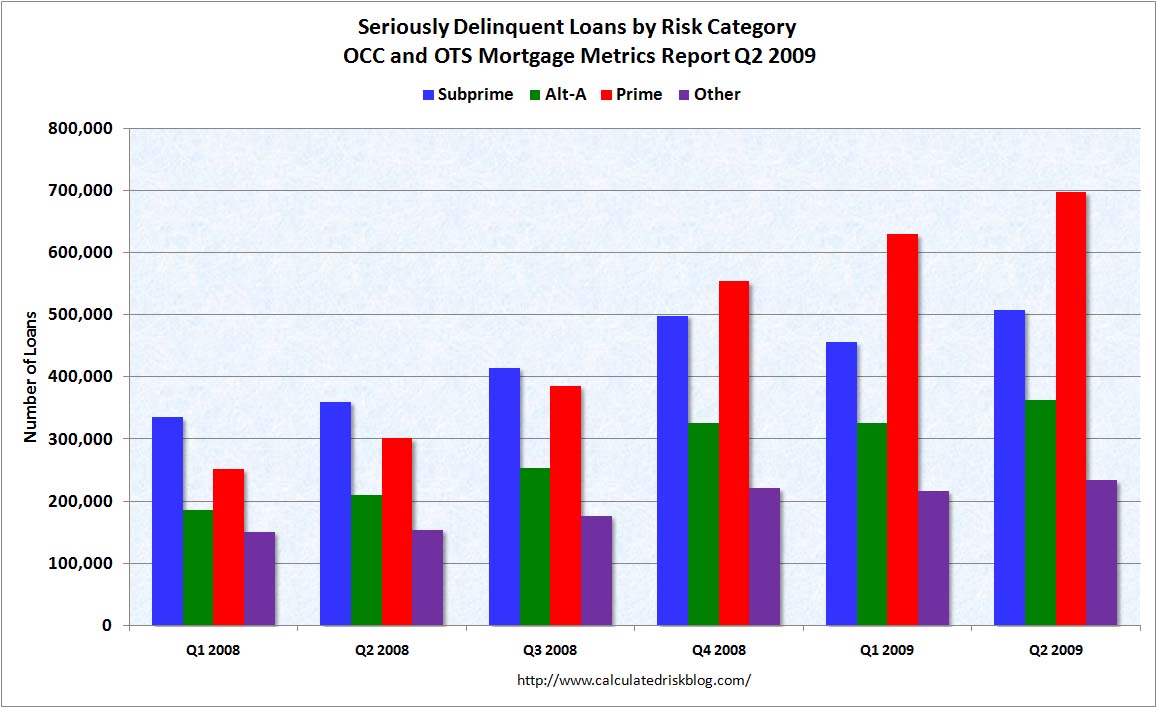

The percentage of current and performing mortgages in the portfolio decreased by 1.4 percent from the previous quarter to 88.6 percent of all mortgages in the portfolio. All categories of delinquencies increased from the previous quarter, with serious delinquencies—loans 60 or more days past due and loans to delinquent bankrupt borrowers—reaching 5.3 percent of all mortgages in the portfolio, an increase of 11.5 percent from the previous quarter. Foreclosures in process reached 2.9 percent of all mortgages, a 16.2 percent increase.

First, keep in mind that “The subprime losses of $150 billion in 2007 required US government aid of $13.2 trillion as of 19 June 2009”. Now, do the math reported above. 88.6 percent of the $6 trillion in mortgages are current. 11.4 percent representing $684 billion are not. Some of those late mortgages will cure, but most will not. Assuming that the 36 percent of mortgages not represented in the report reflect similar percentages, that indicates potential defaults in the realm of $1.1 trillion dollars assuming that the default rate does not continue to rise. The chart below indicates that this is unlikely. Since average losses on foreclosures are reported as $45,000 (Banker & Tradesman) and $60,000 (Freddie Mac), this indicates an average loss per mortgage of around 30 percent, which means that the banking system will have to absorb at least another $330 billion in losses, of which $81 billion is already in process even if no more homeowners fall behind on their mortgages!