“Regulators on Friday shut down a Nevada bank, raising to 83 the number of U.S. bank failures this year. The 83 closures so far this year is more than double the pace set in all of 2009, which was itself a brisk year for shutdowns. By this time last year, regulators had closed 40 banks. The pace has accelerated as banks’ losses mount on loans made for commercial property and development.”

– June 19, 2010, the Associated Press

According to the many expert economists who completely failed to see the financial crisis of 2008 or the subsequent economic contraction coming, the American economy is no longer in a recession but is nearly a year into a recovery. However, it is worth noting that the National Bureau of Economic Research’s Business Cycle Dating Committee, which is the government committee charged with delineating the official beginnings and ends of recessions, has refused thus far to state that the economic contraction that began in 2008 is, in fact, over.

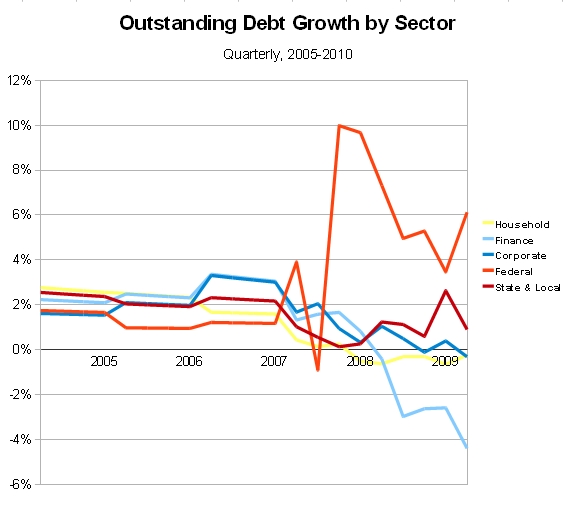

While the GDP figures are positive, other statistics such as the unemployment rate, the velocity of the money supply and the ongoing reduction of debt in the financial and household sectors strongly indicate that the supposed recovery is nothing more than a statistical artifact that is the direct result of a 57 percent increase in outstanding federal debt since the second quarter of 2008. Since government spending is a primary component of the GDP equation, the G in C+I+G+(X-M), literally all of the reported growth in GDP is the result of the increase in outstanding federal debt from $5.2 trillion on June 30, 2008, to $8.3 trillion on March 31, 2010.

Addendum: Here is another piece of evidence that the so-called recovery is nothing more than an artifact of the massive increase in federal borrowing and spending. Notice how far below the average historical 2% increase the three private sectors have fallen and remember that the Finance sector alone is twice as large as the Federal sector.